Pre-tax means before taxes are calculated or deducted. On a paycheck, it usually means money is taken out of your gross pay before certain taxes are applied, which can lower your current taxable income.

Merriam-Webster defines pretax as existing before provision for taxes, and payroll guidance from ADP and FINRA uses the term the same way in employee-benefits and paycheck contexts.

Most people see pre-tax on a pay stub, benefits enrollment form, retirement plan, or payroll deduction summary. In real life, the question is usually not just “what does the word mean?” It is “does this reduce the income I’m taxed on right now?” In many payroll situations, yes. But the exact answer depends on the type of deduction and which tax is being discussed.

This article mainly explains the paycheck meaning, because that is the version most readers are trying to understand. Rules can vary by country, employer, and benefit plan, and the examples below follow the U.S. payroll and benefits framework reflected in IRS, FINRA, and ADP guidance.

Pre-tax meaning in simple terms

In plain English, pre-tax money is handled before tax is applied.

If part of your paycheck is marked pre-tax, that usually means the money comes out before certain taxes are calculated. Because of that, the amount the government taxes right now may be lower than it would be without that deduction.

FINRA explains that every dollar paid toward a pre-tax benefit reduces current taxable income by the same amount for income-tax purposes.

A simple example:

- Gross pay: $2,000

- Pre-tax health insurance deduction: $150

- Pre-tax FSA contribution: $100

- Remaining amount used for the relevant tax calculation: less than $2,000

That does not always mean the money is tax-free forever. In some cases, the tax is simply delayed until later.

What pre-tax means on a paycheck

On a paycheck, pre-tax usually describes a deduction taken from your gross pay before certain taxes are withheld. ADP describes payroll deductions as wages withheld for taxes, benefits, or other obligations, and notes that pretax deductions generally lower taxable income.

That is why a pre-tax deduction can feel “cheaper” than the same deduction taken after tax. The money still leaves your paycheck, but because taxable income may be lower, your take-home pay often drops by less than it would with a post-tax deduction of the same amount. FINRA and ADP both describe this current-tax reduction effect.

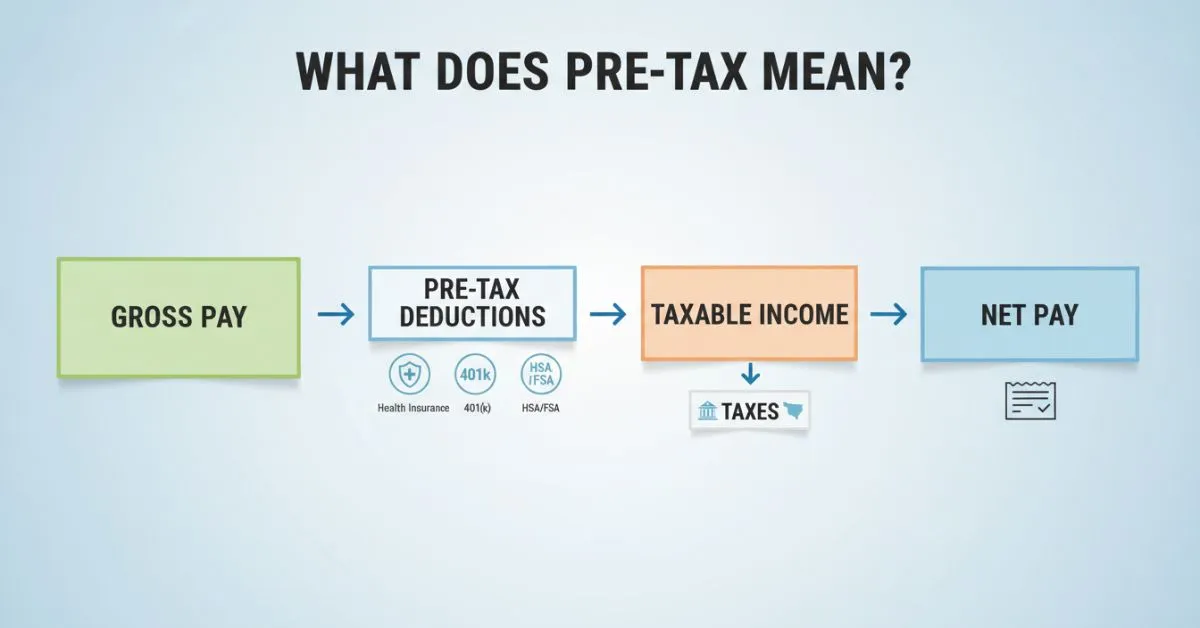

A quick paycheck flow

Gross pay → pre-tax deductions → taxable wages → taxes withheld → net pay

ADP’s payroll explanations center on this same gross-to-net logic: gross pay is what you earn before taxes and deductions, and net pay is what remains after withholding and other deductions are accounted for.

How pre-tax affects taxable income

The biggest practical takeaway is simple:

Pre-tax deductions usually reduce the income that is taxed right now.

That matters because many employees first encounter pre-tax through benefits such as health insurance, FSAs, HSAs through payroll, or retirement contributions. IRS and FINRA guidance both show that these arrangements can reduce current taxable income when set up under qualifying rules.

But there is an important catch: pre-tax does not always reduce every tax. IRS Topic No. 424 says traditional 401(k) elective deferrals generally are not subject to federal income tax withholding at the time of contribution, but they are still included as wages for Social Security and Medicare taxes. That is one of the most misunderstood parts of this topic.

By contrast, the IRS says qualified cafeteria-plan benefits are generally not subject to federal income tax withholding, Social Security, Medicare, or FUTA taxes, though there are exceptions. For example, IRS cafeteria-plan guidance notes that group-term life insurance over $50,000 and adoption assistance have special tax treatment.

Common pre-tax deductions and benefits

These are some of the most common things people mean when they say a deduction is pre-tax.

Health insurance premiums

Employer-sponsored health insurance is often paid on a pre-tax basis through a Section 125 cafeteria plan. The IRS says cafeteria plans let employees use salary reduction agreements to pay for qualified benefits on a pre-tax basis.

Flexible Spending Account (FSA)

A health FSA is one of the clearest examples of a pre-tax benefit. IRS Publication 969 says health FSA contributions are not included in income, and qualified reimbursements are generally not taxed.

Health Savings Account (HSA) through payroll

HSA contributions can also be pre-tax when made through payroll under the right plan structure. IRS Publication 969 explains that employer contributions are not included in income, and HSA contributions made through cafeteria-plan salary reduction can receive favorable tax treatment.

Traditional 401(k)

Traditional 401(k) contributions are commonly called pre-tax because they usually reduce current federal income tax withholding. But again, the IRS says they are still included for Social Security and Medicare wage purposes.

Dependent care assistance

The IRS includes dependent care assistance among the benefits that can be offered through a cafeteria plan. That makes it another benefit readers may see handled on a pre-tax basis, depending on the employer’s plan.

Qualified transportation or commuter benefits

The IRS says a qualified transportation fringe can be excluded from income up to the applicable monthly limit. This is another place where employees may encounter pre-tax treatment, although the exact rules depend on the benefit structure.

Pre-tax vs post-tax vs tax-deferred vs tax-exempt

Many articles stop too early here. These terms are related, but they are not the same.

| Term | What it means | What it usually means for you |

|---|---|---|

| Pre-tax | Money is handled before certain taxes are calculated | Can reduce taxable income now |

| Post-tax | Money is taken out after taxes are applied | Does not reduce current taxable income |

| Tax-deferred | Tax is postponed until later | You may pay tax when money is withdrawn or distributed |

| Tax-exempt | Income or growth may not be taxed if rules are met | Can avoid tax entirely in specific situations |

FINRA distinguishes between pre-tax, tax-deferred, and tax-exempt accounts and warns against treating those labels as interchangeable.

The easiest way to remember the difference

- Pre-tax answers: When is the deduction happening?

- Post-tax answers: Was tax already applied first?

- Tax-deferred answers: Will tax be paid later instead of now?

- Tax-exempt answers: Can this avoid tax under the rules altogether?

Pre-tax vs post-tax: simple real-world example

Imagine two employees each contribute $100 from a paycheck.

- Employee A contributes $100 pre-tax

- Employee B contributes $100 post-tax

Employee A may owe less current income tax because the contribution reduces taxable income first. Employee B pays tax first, then makes the contribution from what is left. That is why pre-tax deductions can change take-home pay differently than post-tax deductions. ADP and FINRA both describe pretax contributions this way.

Common mistakes people make

Mistake 1: Thinking pre-tax means tax-free

It often does not mean that. Traditional retirement contributions may lower taxes now but still create taxable income later. FINRA specifically separates pre-tax from tax-deferred and tax-exempt for this reason.

Mistake 2: Assuming every pre-tax deduction lowers every tax

That is not true. The IRS says traditional 401(k) deferrals generally reduce current federal income tax withholding, but they are still wages for Social Security and Medicare taxes.

Mistake 3: Assuming all benefit accounts work the same way

They do not. IRS Publication 969 treats HSAs, FSAs, HRAs, and MSAs differently, and the rules around contributions, employer funding, and tax treatment are not identical.

Mistake 4: Forgetting that “pre-tax” can have other meanings

In business or accounting, pretax earnings means profit before income taxes are subtracted. Merriam-Webster also gives examples such as pretax earnings, pretax salary, or pretax sales. That is a valid meaning, but it is not usually the main intent behind this query.

What Most Articles Miss About This Topic

The most overlooked point is that pre-tax is not one single tax rule. It is a timing concept. It tells you the money is being handled before a relevant tax calculation, but it does not automatically tell you which taxes are reduced and which are not. IRS guidance makes this clear with 401(k) deferrals versus cafeteria-plan benefits.

Another thing many pages skip is that pre-tax and tax-deferred are not identical. A traditional 401(k) contribution is commonly described as pre-tax when it goes in, but it is also tax-deferred because tax is generally paid later when the money comes out. FINRA treats those as related but distinct ideas.

A third missed detail is that Section 125 cafeteria plans do a lot of the real work behind common pre-tax benefits. The term sounds simple on the surface, but many paycheck deductions are only pre-tax because they are offered through a qualifying employer plan with specific tax treatment rules.

FAQ

Does pre-tax mean before taxes are taken out?

Yes. In ordinary use, pre-tax means before taxes are calculated or deducted. On a paycheck, it usually refers to deductions taken before certain taxes are applied.

Does pre-tax lower taxable income?

Usually, yes. Pretax deductions generally lower current taxable income, though the exact tax effect depends on the deduction and the tax involved.

Is pre-tax the same as post-tax?

No. Pre-tax deductions happen before certain taxes are calculated. Post-tax deductions happen after taxes have already been applied.

Is a traditional 401(k) pre-tax?

Usually yes for current federal income tax withholding, but IRS guidance says those deferrals are still counted as wages for Social Security and Medicare taxes.

Are health insurance premiums pre-tax?

They often are when offered through a cafeteria plan, but the exact treatment depends on the employer’s plan and the benefit involved.

Are HSA and FSA contributions pre-tax?

They often can be through payroll under qualifying plan rules. IRS Publication 969 explains the tax-favored treatment for both.

Is pre-tax the same as tax-free?

No. Some pre-tax arrangements reduce taxes now but may still be taxed later. Tax-free or tax-exempt treatment is a different concept.

Final takeaway

If you see pre-tax on a paycheck, the safest interpretation is this: the money is being handled before certain taxes are calculated, which may lower the income taxed right now. The smart next step is to check what the deduction is, which taxes it affects, and whether the tax is avoided now or merely delayed until later. IRS, FINRA, and ADP guidance all point to that more precise, practical reading.

Click Below To Read About These Posts:

Blue Rose Meaning: Blue Roses Symbolize in Love, Gifts, and Life

What Does La Dolce Vita Mean? Translation, Real Meaning

What Does “Bye Felicia” Mean? Complete Explanation

Hi, I’m Clara Lexis from Meanvia.com. I break down words and expressions so they’re easy to understand and enjoyable to learn. My mission is simple: make language approachable and fun, one word at a time.